CME received an advance briefing at the annual State Budget ‘lock-up’, joining many other key industry association representatives. This year’s presentation was provided by the Premier, his first as Treasurer.

The tone was bullish and stressed the strong performance of WA in comparison to other Australian and international jurisdictions on measures such as net debt (lowest ratio in the nation at 60 per cent), low unemployment and high participation, consumer and business confidence. ANZ bank data, for example, showed WA household spend eclipsing the rest of the nation.

The Premier credited ‘short and sharp’ lockdowns and WA’s ability to keep the virus at bay for much of this success and outlined his plan to continue investing in the COVID-19 response and recovery. In anticipation of other states and territories preparing to report large deficits, the Premier noted he would continue to push back on inevitable calls to claw back WA’s hard-won 70 per cent floor on Commonwealth GST grants.

CME analysed the Budget following the lock-up, releasing detailed commentary here:

Forecasting iron ore prices and royalty revenue

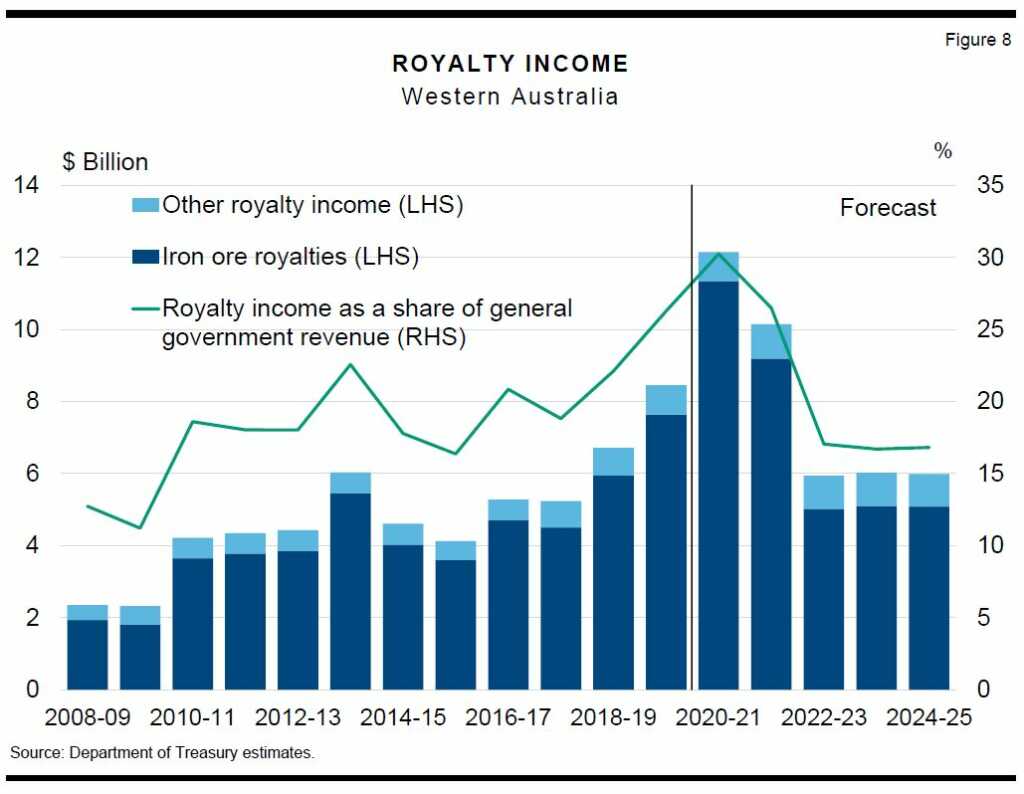

Since the Brazil tailings dam disaster in 2019, global iron ore supply has been slow to recover, allowing WA to achieve record exports of iron ore at elevated prices during the COVID-19 pandemic. State coffers received $11.3 billion in royalty revenue from iron ore alone in 2020-21.

Royalty revenue from iron ore is expected to decline going forward, with the WA Department of Treasury prudently estimating a drop in collections of more than half – to $5.0 billion per annum from 2022 onwards. This is a conservative forecast compared to pre-COVID-19 receipts: $4.5 billion in 2017-18 and $5.4 billion in 2018-19. Given forecast errors in past Budget years have been as large as 47 per cent, it makes sense for Treasury to be incredibly careful in assuming prices and volumes in a volatile market, as the world emerges from the uncertainties of COVID-19.

Royalty income from lithium production is expected to more than offset the decline in gold and copper productions as mines reach their end of life in 2023-24. Prices for lithium spodumene and nickel have been revised upwards in anticipation of heightened demand for electric vehicles. Treasury is expecting royalty revenue from lithium to surpass pre-COVID-19 receipts: $94 million in 2017-18 vs $113 million in 2024-25.

Paying head contractors within 20 business days

Member companies will be expected to get their payment practices for new construction contracts up to code by 1 August 2022. The first stage of the new Security of Payment laws will take effect, providing a rapid dispute resolution process and improved protection for subcontractors. The second stage of retention trust schemes will commence in February 2023, followed by progress on retention funds in February 2024.

Supporting regulations will be released for consultation as early as Q1 2022. Member companies wishing to be included in the CME industry submission should join the Economics & Productivity Committee. Further details on the government’s action plan can be found here.

Contact: Linh Nguyen, Policy Adviser – Industry Competitiveness

Email: l.nguyen@cmewa.com